Rwanda’s foreign exchange reserves are expected to rebound to $2.2 billion in 2026, marking a recovery after a projected decline in 2025, according to the latest economic outlook.

The rebound follows a projected decline in reserves from $2.4 billion in 2024, equivalent to 5.3 months of import cover, to about $1.8 billion in 2025, or 3.7 months of imports.

By 2026, reserves are expected to recover to cover approximately 4.3 months of imports, returning above the widely accepted adequacy threshold of four months. In the years beyond, reserves are projected to stabilise around $2.6 billion, supported by sustained inflows of foreign direct investment and concessional financing.

External pressures and recovery path

The short-term deterioration in Rwanda’s external position is tied to a projected rise in the current account deficit to 13.3 percent of GDP in 2026, up from 12.9 percent in 2025. This reflects strong import demand as the country invests in long-term growth projects.

“This increase is driven by a surge in imports of capital goods, linked to key projects like a new airport, and intermediate goods. While strong export performance and supportive policy measures are projected to improve the current account balance in the near term, gradually,” reads the Annual Economic Report for the Fiscal Year 2024/2025 published by the Ministry of Finance and Economic Planning.

However, the outlook remains optimistic. Strong export performance, particularly in commodities such as coffee and minerals, alongside supportive policy measures, is expected to gradually ease external imbalances.

Recent data shows an improvement in Rwanda’s external position, with the overall balance of payments surplus rising from about $217 million in the Financial Year 2023/24 to $274 million, supported by stronger inflows from exports, investment, and financing.

Gold emerges as a strategic reserve asset

A notable development shaping the forward outlook is Rwanda’s move to diversify its reserves. The National Bank of Rwanda has begun purchasing gold as part of its reserve assets, marking a shift toward strengthening resilience against global financial volatility.

Gold is widely regarded as a stable store of value that does not easily depreciate, especially during periods of currency fluctuations or global uncertainty. By incorporating gold into its reserves, Rwanda is positioning itself to reduce reliance on traditional foreign currency holdings such as the US dollar while enhancing long-term stability.

The central bank is expected to disclose the volume of gold accumulated, a move that could provide further insight into the country’s evolving reserve management strategy.

What it means for the economy

Foreign reserves play a critical role in stabilising the economy. When reserves are sufficient, they enable the country to pay for essential imports, support the national currency, and cushion against external shocks.

If reserves fall too low, the Rwandan franc could come under pressure, making imports more expensive and increasing the cost of living. Conversely, the projected recovery in reserves is expected to help stabilise the exchange rate, contain imported inflation, and support purchasing power.

The central bank also retains the ability to intervene in currency markets using reserves, injecting foreign currency when needed to limit excessive depreciation.

The National Bank of Rwanda (BNR) has begun purchasing gold as an additional way of building and diversifying its reserves.

Analysts warned that even brief interruptions of passage ripple through global markets and that prolonged instability risks evolving into a broader inflation and growth crisis.

Roughly 20 percent of global oil and liquefied natural gas passes through this narrow corridor linking the Gulf to global markets, making it one of the world’s most critical energy chokepoints. Shocks of this magnitude propagate rapidly through trade, finance and consumption, ultimately affecting household budgets across economies worldwide.

Largest oil supply disruption

Amid escalating geopolitical tensions, flows through the Strait of Hormuz have become increasingly volatile.

Data from shipping analytics firms show that prior to the escalation, an average of 45-50 oil tankers transited the strait each day. In the weeks since, that number has dropped by more than half, with fewer than 20 vessels transiting daily, and at times of heightened tension, falling to near zero as shipping temporarily halted.

Russell Hardy, CEO of Vitol, the world’s largest independent oil trader, warned that the market will lose at least 1 billion barrels of crude and refined products due to the crisis.

He noted that sustained attacks on Gulf energy infrastructure and repeated closures of the strait have already removed some 12 million barrels per day of production since late February. Analysts expected the global oil market to shift from an expected surplus into a deficit of about 750,000 barrels per day in 2026.

Fatih Birol, executive director of the International Energy Agency (IEA), said the war in the Middle East “is creating a major energy crisis, including the largest supply disruption in the history of the global oil market,” warning that without a swift resolution, impacts will intensify.

In response, the IEA has coordinated an emergency release of around 400 million barrels from strategic reserves in March, the largest ever, to stabilize markets.

Brent crude, the international benchmark, rose 63 percent in March, surpassing the 46 percent monthly gain recorded in September 1990 during the first Gulf War. Analysts estimate sustained instability could keep Brent crude between 100 and 190 U.S. dollars per barrel, with an average above 130.

Meanwhile, the shock is reshaping global flows. The London-headquartered maritime analytics firm Windward noted that crude shipments are increasingly rerouting toward the Gulf of Mexico, positioning the United States as a key export anchor amid Hormuz disruptions.

U.S. producers could benefit from higher prices, even as import-dependent economies bear the costs, analysts were quoted by Al Jazeera as saying.

“Conflict tax”

If the first layer of impact unfolds in supply, the second is felt in daily life. Reports point to a widening “conflict tax.”

The International Monetary Fund (IMF) identified energy as the main transmission channel, noting that for fuel-importing economies, rising prices act like a sudden tax on income.

Recent data showed these pressures are increasingly visible at the fuel pump. In the United States, gasoline prices rose by more than 24 percent in March alone, contributing significantly to a surge in retail spending driven largely by higher fuel costs.

In Asia, higher fuel and electricity costs are squeezing manufacturing output and household purchasing power, and in Europe, the crisis revives memories of the 2021-2022 gas shock. British officials warn that elevated food and energy prices could persist for months even after the conflict ends, reflecting delayed inflationary effects.

The real-world impact in other respects is increasingly visible. The war in the Middle East has triggered a sharp rise in air fares, with the lowest-priced economy tickets costing, on average, 24 percent more than a year ago, according to new research from the consultancy Teneo. The report said airspace restrictions linked to the conflict have forced airlines to reroute numerous flights, increasing fuel consumption and pushing up operating costs.

At the micro level, the consequences are equally tangible. In Ethiopia, a wholesale trader told Xinhua that fuel shortages delayed shipments by several days, causing goods to spoil and resulting in financial losses. In Portugal, consumers reported rising grocery bills eroding incomes, reflecting a broader cost-of-living strain.

“Even if the war is far away, the effect reaches people’s daily lives very quickly,” said Tiago Santos, a Brazilian immigrant working as a salesman in Lisbon, Portugal, capturing how geopolitical shocks in energy markets translate into lived economic pressure far beyond the region of conflict.

Structural adjustments

Beyond immediate shocks, analysts have pointed to longer-term changes. Restoring oil production to pre-conflict levels will likely take several months, depending on the extent of damage to oilfields and how smoothly shipping through the Strait of Hormuz resumes.

Even under a relatively constructive scenario, the Australia and New Zealand Banking Group (ANZ) analysts estimate that only 2-3 million barrels per day could return in the first month, with another 2-3.5 million barrels per day gradually coming back over the rest of the second quarter. However, they stressed that operational disruptions, damaged infrastructure and export bottlenecks mean the recovery will not be smooth or linear.

At a systemic level, the crisis is accelerating a reconfiguration of global energy and trade networks. Windward reported that alternative logistics patterns, notably overland transport corridors and destination shifts, are becoming increasingly normalized rather than temporary responses.

“This architecture is unlikely to unwind quickly, even if the ceasefire holds,” the report noted, adding that war-risk insurance, backlog pressure, congestion risk and unresolved transit governance mean that the current system has already moved from improvisation into operational normalization.

More broadly, the crisis highlights the vulnerability of maritime chokepoints and is prompting countries to diversify supply sources, expand strategic reserves and rebalance efficiency with resilience in global trade systems.

At the same time, the shock is reshaping the trajectory of the energy transition. Policymakers across regions have called for faster deployment of clean energy to reduce exposure to similar shocks.

South Korean President Lee Jae Myung has recently urged a rapid, large-scale transition toward renewables. European Commission President Ursula von der Leyen has called for speeding up “the integration of low-carbon, home-grown energy” to strengthen energy security.

“This fossil fuel crisis will happen again and again,” said UN Climate Change Executive Secretary Simon Stiell. “Sunlight does not depend on narrow and vulnerable shipping straits. Wind blows without massive taxpayer-funded naval escorts.”

Analysts warned that even brief interruptions of passage ripple through global markets and that prolonged instability risks evolving into a broader inflation and growth crisis.

The report, published on Tuesday, shows a significant increase from 612 projects recorded in 2024, with the new investments expected to generate more than 38,000 jobs. Real estate, manufacturing and mining accounted for the largest share of the registered investments, underlining continued investor confidence in Rwanda’s economic outlook.

Foreign private capital performance also remained strong. According to the 2025 Foreign Private Capital survey, Foreign Direct Investment inflows rose to $872.9 million (Rwf 1.27 trillion) in 2024, marking a 21.8 percent increase from $716.5 million (Rwf 1.04 trillion) recorded in 2023.

RDB said the combined performance demonstrates sustained confidence in Rwanda’s policy environment and its ability to support investors beyond promotion through implementation and service delivery.

Tourism remained one of the country’s strongest-performing sectors, with revenues reaching $685 million (Rwf 997.9 billion) in 2025, up from $647 million (Rwf 942.6 billion) in 2024, representing a 6 percent year-on-year increase.

Visitor arrivals also rose by 9 percent to 1.49 million, supported by Rwanda’s flagship gorilla trekking experiences and expanded tourism offerings across the country’s national parks.

The Meetings, Incentives, Conferences and Exhibitions (MICE) segment generated $94.7 million (Rwf 137.9 billion), up from $84.8 million (Rwf 123.5 billion) in 2024, reflecting an 11 percent increase. The growth was driven by 165 international and regional events hosted in Rwanda during the year.

Among the major events were the UCI Road World Championships held in September, the first time the global cycling championship was hosted in Africa, alongside Move Afrika Kigali featuring John Legend, the Mobile World Congress, and Season 5 of the Basketball Africa League.

RDB said these events played a major role in boosting visitor arrivals, raising Rwanda’s international profile, and strengthening the country’s MICE ecosystem.

Rwanda’s export sector also remained resilient, with total export receipts reaching $3.6 billion, supported by steady performance in mining, agriculture and horticulture. Services exports increased by 2.7 percent year-on-year, while air cargo volumes rose by 2.4 percent to 6,257 tonnes from 6,113 tonnes in 2024.

The country also continued to leverage global sports partnerships under the Visit Rwanda campaign to strengthen international visibility and attract high-value tourism and investment.

In 2025, Rwanda renewed its partnership with Paris Saint-Germain until 2028 and signed a new three-year deal with Atlético de Madrid running through 2028.

It also expanded long-term sponsorship agreements with the Los Angeles Clippers and the Los Angeles Rams, both extending through 2030.

These partnerships are expected to increase Rwanda’s global exposure, attract more high-value visitors and investors, and support further growth in tourism and the MICE segment.

The report also highlighted Rwanda’s strong performance in global rankings, including the World Bank B-READY Report, where the country achieved Africa’s highest score on regulatory framework performance.

Rwanda also maintained its position as one of Sub-Saharan Africa’s top performers in the World Justice Project Rule of Law Index.

To improve the business environment, RDB said it continued expanding the One Stop Centre and digitising services through a unified platform expected to provide more efficient and transparent access to over 400 services delivered by more than 20 institutions.

A real-time performance monitoring system was also introduced to improve service delivery in areas such as business registration and investment facilitation.

Additionally, Rwanda established the National Lottery and Gambling Commission under RDB’s mandate to regulate the gambling sector and strengthen governance, compliance and oversight.

Commenting on the results, RDB Chief Executive Officer Jean-Guy Afrika said the performance reflects continued progress in supporting Rwanda’s economic fundamentals.

“The 2025 performance reflects continued progress in supporting Rwanda’s economic fundamentals and delivering on our priorities across investment, exports, tourism and service delivery. We remain focused on building a predictable and competitive environment that enables private sector growth and long-term development,” he said.

RDB said it will continue implementing the Second National Strategy for Transformation (NST2) and its 2025–2030 strategy, with a focus on expanding investment, strengthening exports, promoting high-value tourism and advancing innovation.

Rwanda registered $2.62 billion (approximately Rwf 3.8 trillion) in investments across 799 projects in 2025, reflecting stronger economic momentum driven by growth in investment, tourism, exports and business reforms, according to the latest annual report released by the Rwanda Development Board (RDB).

The fund, named the Rwanda SME Growth Fund, is a joint initiative between the Rwanda Social Security Board (RSSB) and Enko Capital. It was officially unveiled in Kigali on April 27, 2026, following the signing of a partnership agreement between the two institutions.

Under this arrangement, RSSB will provide the capital, while Enko Capital will be responsible for evaluating investment proposals and managing the fund’s portfolio.

The fund begins with an initial capital of $30 million (over Rwf 43 billion), with plans to expand to $100 million in the coming years. In addition to this investment, RSSB has set aside an extra Rwf 3 billion to support operational activities, including deploying skilled professionals to assist companies receiving funding.

This additional support is intended to help businesses address capacity gaps—for instance, by enabling them to recruit essential staff needed during expansion phases.

Unlike traditional financing mechanisms, the Rwanda SME Growth Fund will not offer grants or loans. Instead, it will take equity stakes in eligible businesses. Companies with viable and scalable projects will receive capital in exchange for a shareholding structure, where part of the ownership is transferred to the fund for a defined period of between five and ten years.

The Director General of RSSB, Rugemanshuro Regis, said the fund is designed to accelerate the growth of private SMEs. He noted that RSSB is also seeking additional partners to help raise the fund’s total value to $100 million.

He explained that many local industries operate below capacity, often between 40% and 50%, despite producing goods in high demand. He attributed this to the high cost and limited accessibility of bank loans, which the fund aims to address.

According to him, many entrepreneurs lack sufficient collateral to meet bank requirements, making it difficult to secure financing. As a result, businesses remain under-capitalized, limiting their production capacity and contributing to increased imports.

Businesses seeking funding will be required to submit detailed information about their operations and investment needs to Enko Capital.

Each company will be eligible to receive between $500,000 and $5 million from the fund.

RSSB indicated that after a period of five to ten years, the fund will exit its investment by selling its shares either back to the company or to other investors, depending on the growth achieved.

Co-Founder and Managing Partner at Enko Capital, Cyrille Nkontichou, emphasized that access to affordable capital remains a major challenge for SMEs, particularly due to high borrowing costs and strict lending conditions.

He noted that many SMEs lack collateral and require longer repayment periods, which often do not align with the terms offered by financial institutions. In this context, the Rwanda SME Growth Fund presents a more flexible and sustainable financing solution.

Nkontichou added that Enko Capital already operates in several African countries, managing assets worth approximately $1.7 billion. He described the firm’s expansion into Rwanda as a strategic opportunity, not only to implement this fund but also to tap into the country’s growing investment landscape.

According to the Ministry of Trade and Industry, SMEs account for 98% of all businesses in Rwanda and employ around 2.5 million people, highlighting their critical role in the country’s economy.

The fund was officially unveiled in Kigali on April 27, 2026, following the signing of a partnership agreement between the two institutions. The fund was unveiled in Kigali through a partnership between RSSB and Enko Capital.The Director General of RSSB, Rugemanshuro Regis, said the fund is designed to accelerate the growth of private SMEs.Co-Founder and Managing Partner at Enko Capital, Cyrille Nkontichou, emphasized that access to affordable capital remains a major challenge for SMEs, particularly due to high borrowing costs and strict lending conditions.

The Rwanda Utilities Regulatory Authority (RURA) has sanctioned internet service provider GVA Rwanda Ltd, commonly known as CanalBox, following days of widespread service disruptions that affected customers across Rwanda.

In a statement issued on Monday, April 27, RURA said the company had been penalised under Article 269 of Law No. 24/2016 for continued non-compliance with service standards. The regulator ordered CanalBox to compensate all customers affected between April 13 and April 20, 2026, and to pay daily penalties until it fully restores stable service.

Additionally, the company has been instructed to submit regular progress reports within prescribed timelines. RURA emphasised that it will closely monitor the operator’s compliance, warning that failure to meet requirements could lead to further regulatory action.

“GVA has committed to compliance, and RURA will continue to closely monitor progress to ensure full service stability. Failure to comply will result in further regulatory action,” RURA announced.

The sanctions follow earlier enforcement steps taken by the regulator. On April 21, RURA summoned CanalBox management after receiving numerous complaints about poor internet connectivity. The company was invited to a formal hearing to explain the disruptions and outline corrective measures.

The disruptions were initially linked to a major fiber optic fault with their international provider overseas, which impacted stability and speeds across their network.

The Rwanda Utilities Regulatory Authority (RURA) has sanctioned internet service provider GVA Rwanda Ltd, commonly known as CanalBox, following days of widespread service disruptions that affected customers across Rwanda.

While many of these projects have traditionally been driven by experienced investors, a growing number of young entrepreneurs are stepping into the real estate sector, answering national calls to play a more active role in development.

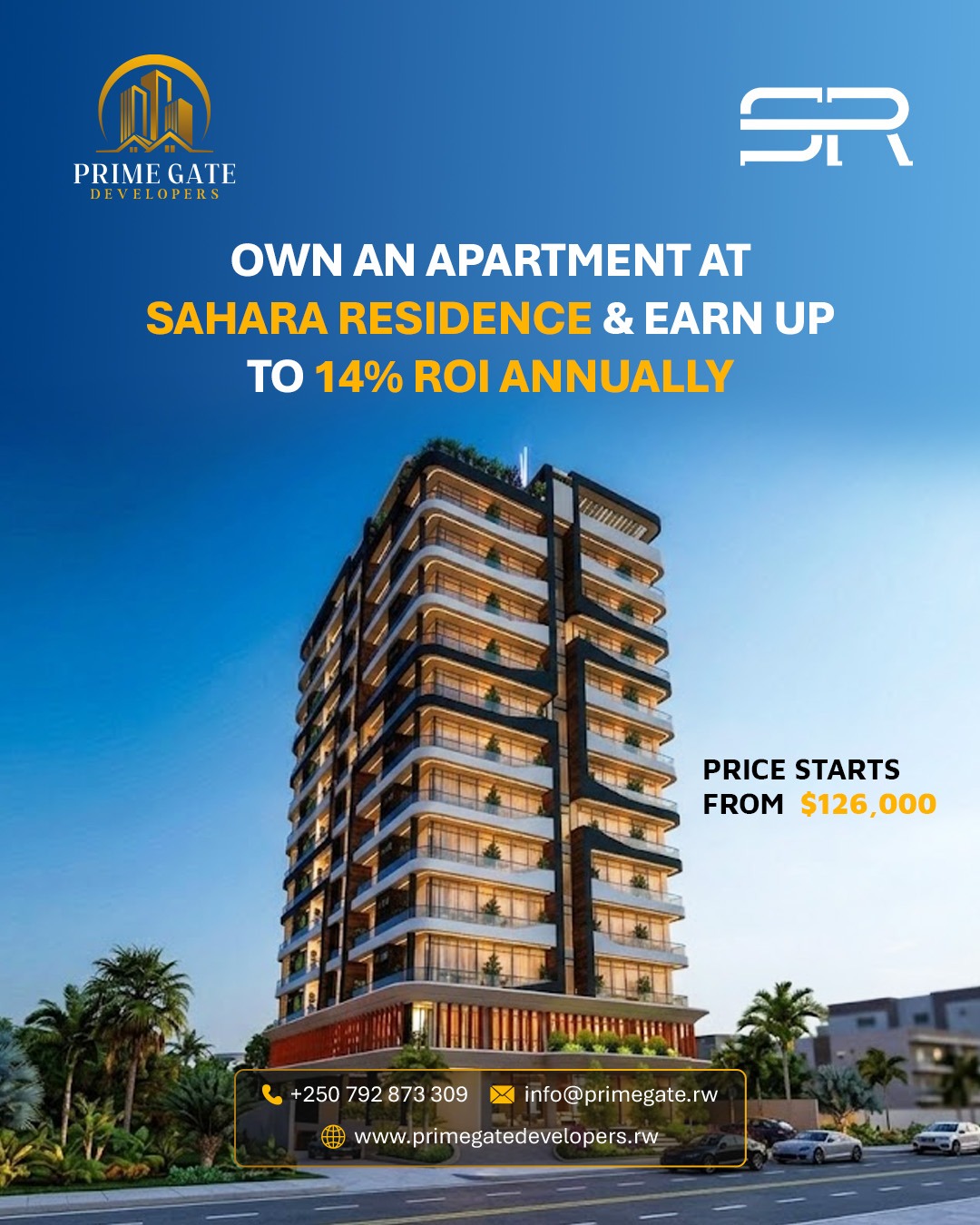

Among them is Prime Gate Developers, a company represented by engineer Delphin Tuyishime. Working with a team of young professionals, the firm has launched an ambitious housing project known as Sahara Residence.

The 12-storey building is being constructed near Lemigo Hotel, just five minutes from Amahoro Stadium and about 10 minutes from the city centre.

Tuyishime, who chairs the company’s board, partnered with Augustin Kabandana and investor Gerard Mpyisi to bring the project to life. Construction officially began on April 25, 2026.

Explaining what inspired the idea, Tuyishime pointed to the role locals often play in projects initiated by foreign investors.

“I noticed that foreigners come here to invest, and we are the ones implementing their projects. In the end, they benefit from ideas that originate from us,” he said.

He added that his experience in Dubai, where the housing sector is highly developed, pushed him to think about applying similar concepts back home.

“Having seen how advanced real estate is in Dubai, I told myself we should be doing the same in our country. That’s when I reached out to partners and we began working on how to make this project a reality,” he explained.

For Gerard Mpyisi, the project was not immediately convincing. “To be honest, when they first presented the idea to me, I thought it was impossible,” he said. “I challenged them to go and secure all the required construction permits, and within a short time, they came back with everything ready.”

He revealed that the land where the building is being constructed had originally been reserved for his family, but they eventually agreed to repurpose it.

“My family didn’t understand it at first when I told them the property would be redeveloped. But when I showed them what was planned here, they accepted without hesitation. In two years, you will see an outstanding building on this site,” he said.

Prime Gate Developers currently employs more than 40 young professionals under the age of 30, working in areas such as architectural design, marketing, and technology. The company is led by CEO Dr. Egide Igabe, who previously played a role in introducing electric public transport during his time at Volcano Express.

The Rwanda Housing Authority (RHA) has welcomed the initiative, describing it as aligned with national housing priorities.

“We need more investors like Prime Gate Developers, especially those focusing on residential housing,” said RHA Director General Alphonse Rukaburandekwe. “Under NST2, we are required to build over 500,000 housing units. As RHA, we are committed to working with investors to ensure Rwandans have access to quality, well-regulated housing.”

Residents of Sahara Residence will enjoy views of different parts of Kigali.

What Sahara Residence will offer

Sahara Residence is designed as a mixed-use development. The ground floor and first level will accommodate commercial spaces, including restaurants, offices, and retail outlets.

Located in Kimihurura, the building sits close to the Kigali Convention Centre, one of the city’s key business hubs.

From the second to the 12th floor, the building will feature modern apartments equipped with essential amenities, including spacious living areas, fitted kitchens, and en-suite bedrooms.

Residents will also have access to a swimming pool, a fully equipped gym, and ample parking. In total, the development includes 111 units, with 101 available for sale. About 70% have already been purchased, with the remaining units expected to be sold within a month.

Investment in the property starts at $126,000. Buyers can make an initial payment of between 20% and 30%, with the remaining balance payable in installments of 1%.

According to the developers, the project offers an annual return on investment ranging between 12% and 18%, positioning it as both a residential and investment opportunity.

The company says its team remains available to provide guidance and detailed information to interested investors through its official channels.

Sahara Residence will have 12 floors.Sahara Residence will be among the high-rise buildings in Kigali. Residents of Sahara Residence will enjoy views of different parts of Kigali.Prime Gate Developers is set to construct a building that will enhance Kigali’s skyline.Each apartment in Sahara Residence will have a spacious living room.The apartments include a designated dining area.The residential units will come fully equipped with essential amenities.Early buyers will have the opportunity to customize the interior design of their units.One-bedroom units will include modern beds.A ground-floor area in Sahara Residence is designated for a restaurant. Sahara Residence will feature a fully equipped gym.There is dedicated space for various business activities.The lower section is reserved for restaurants and other commercial activities.Gerard Mpyisi is among the key partners in the construction of Sahara Residence and other projects by Prime Gate Developers.Gerard Mpyisi said the determination shown by the youth convinced him to support them. Prime Gate Developers has several projects aimed at transforming housing in Kigali. Eng. Delphin Tuyishime emphasized the need for Rwandans to invest in real estate Prime Gate Developers aims to build residential housing in different parts of Kigali. Gerard Mpyisi said the project has been thoroughly planned and will be completed within a short time.

Alphonse Rukaburandekwe shared details about the standards for modern building design. Construction of Sahara Residence is expected to take two years. Sahara Residence is expected to contribute to the NST2 development programme.Gerard Mpyisi and Alphonse Rukaburandekwe launched the construction of Sahara Residence.Eng. Delphin Tuyishime presented the construction idea to Gerard Mpyisi.Flavia Bwiza is the head of sales and marketing at Prime Gate Developers.Chairman Eng. Delphin Tuyishime and CEO Dr. Egide Igabe of Prime Gate Developers.Investors in Sahara Residence are promised attractive and timely returns.Alphonse Rukaburandekwe pledged support to Prime Gate Developers.Dr. Egide Igabe assured partners of transparent operations. RHA Director General Alphonse Rukaburandekwe, Prime Gate Developers CEO Egide Igabe, and investor Gerard Mpyisi, a key partner in the project. The site for Sahara Residence has already been prepared for construction.Augustin Kabandana is a member of the Board of Prime Gate Developers.

Data from the Rwanda National Police Fire and Rescue Brigade shows that between 2020 and March 2025, the country recorded 1,118 fire incidents linked to various causes. The number of cases has generally increased over the years, rising from 136 in 2020 to 362 in 2024.

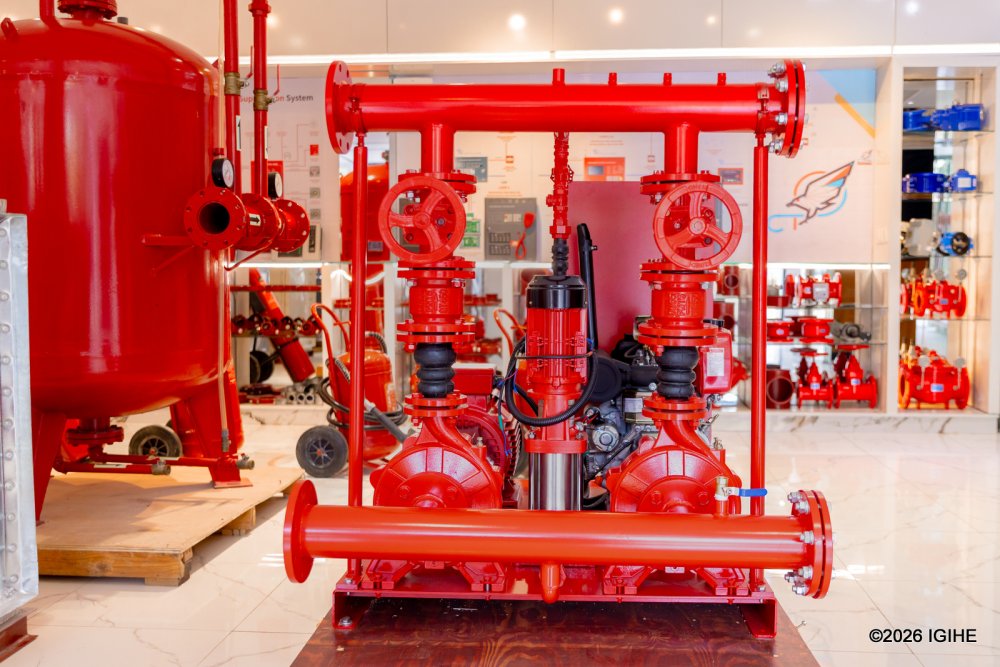

Fire response largely depends on specialized equipment such as fire extinguishers, most of which are currently sourced from abroad.

Habimana, who owns Cyusa Technology Africa, a company dealing in fire safety equipment, now plans to shift toward local production.

Construction of the factory is expected to begin in 2027, with operations projected to start by late 2028. The project, valued at Rwf 5 billion, is set to create around 400 jobs. It will be located in Jabana Industrial Zone in Gasabo District.

Speaking to IGIHE, Habimana said preparations are already underway, including land acquisition and design planning.

“We have secured two hectares in Jabana for the factory. We are also working with our partners in China, where we currently source some equipment, and we are finalizing the plant’s design,” he said.

He explained that the factory will initially focus on assembling fire extinguishers using imported components, with plans to build a strong local supply chain over time. With an already established client base, he believes the factory will provide a reliable local alternative to imported equipment.

In addition to supplying fire safety equipment, Cyusa Technology Africa offers services such as designing fire prevention systems, installing equipment, and assessing safety needs for institutions.

The company has previously worked with several prominent establishments, including the National Bank of Rwanda, Rwanda Airports Company, Kigali Heights, Marriott Hotel, and Four Points by Sheraton.

Habimana’s planned factory aims to cut reliance on imported fire safety equipment.The new plant could improve access to fire-fighting equipment across Rwanda.Habimana eyes local market with Rwf 5bn fire equipment investment.Cyusa Technology Africa offers services such as designing fire prevention systems, installing equipment, and assessing safety needs for institutions.

“We used to hide from them,” said Qi Pengxiao, now in his 80s. He arrived in the Qaidam Basin in Qinghai Province as an oil worker in 1957, when the resources beneath the ground were the only treasures that mattered. “Now they’ve become our precious assets: new energy.”

Today, under that same sun, row upon row of solar panels stretch across the desert like a blue ocean, while towering turbines turn in a slow, steady rhythm in the wind. The barren land has emerged as a new energy heartland of renewables.

Driving this shift is a revolution spanning over a decade championed by Chinese President Xi Jinping, who aims to build a new energy system that is clean, low-carbon, secure and efficient to power the world’s second-largest economy.

Xi, also general secretary of the Communist Party of China (CPC) Central Committee and chairman of the Central Military Commission, has long given priority to energy security, an issue he considered overarching and strategic to the nation’s economic and social development.

“Whoever commands energy may well command the development potential and the vital source of wealth creation,” Xi told a meeting on fiscal and economic affairs back in 2014.

In the face of changes in energy demand and supply, as well as new developments in the international energy landscape, China must ensure national energy security through a revolution in energy production and consumption, he said.

Central to his thinking is a question of balance. How to advance the transition from fossil fuels to new energy without undermining the energy security on which China’s development depends, while steadily improving self-sufficiency and long-term supply resilience? The country’s climate goals — to peak carbon emissions before 2030 and achieve carbon neutrality by 2060 — only sharpen the stakes.

The solution is taking shape in the vast fields of solar panels, an expanding power grid, and a growing fleet of electric vehicles. China now relies on an increasingly diverse energy mix. While crude oil output remains steady at around 200 million tonnes a year, its wind and solar energy installations for the first time surpassed those of thermal power in 2025.

This restructuring has not come at the expense of energy security. Despite growing demand in recent years, over 90 percent of China’s increase in energy consumption has been met domestically, and one-third of its electricity consumption is powered by green energy.

During an inspection trip last month to Xiong’an New Area, a much-anticipated “city of the future” in north China’s Hebei Province, Xi said China’s efforts to develop wind and solar power had proven “forward-looking in hindsight.”

At the same time, he noted, coal-fired power remains the bedrock of the nation’s energy system, providing a crucial foundation to ensure energy security.

Such a coordinated approach has led to significant gains in energy efficiency. From 2013 to 2023, China fueled 6.1 percent average annual economic growth with just 3.3 percent energy consumption increase, making it one of the world’s fastest-improving nations in energy intensity.

China is also strengthening its energy infrastructure. Today, it takes only an instant — about five milliseconds, to be exact — for electricity generated in the northwestern Qinghai Province to travel over 1,500 kilometers and reach the power-intensive central China via ultra-high-voltage lines. A single second’s pulse of electricity is enough to support a household in Henan Province — one of the country’s most populous regions and an economic powerhouse — for an entire year.

In Henan alone, the ultra-high-voltage corridor is estimated to help slash the region’s annual coal consumption by over 15 million tonnes, cutting carbon dioxide emissions by more than 25 million tonnes.

The sweeping transformation is underpinned by a wave of technological breakthroughs that Xi has called for, not only to advance the energy transition but also to foster new engines of economic growth.

“We should develop energy technology and its related industries into a new growth driver to boost industrial upgrading, facilitating the development of new quality productive forces,” he has told senior CPC officials.

China has emerged as a global frontrunner in new energy technology and equipment manufacturing. From 2021 to 2025, the nation held over 40 percent of the world’s new energy patents, while its photovoltaic conversion efficiency and offshore wind turbine unit capacity repeatedly set new world records.

Just a day earlier, on April 21, Chinese clean-tech giant Contemporary Amperex Technology Co., Ltd. (CATL) unveiled its third-generation Shenxing fast-charging battery, capable of charging from 10 percent to 98 percent in six minutes and 27 seconds, narrowing the gap between electric vehicle charging and conventional refueling.

In the recently adopted outline of the 15th Five-Year Plan (2026-2030) for national economic and social development, China has set a bold target of doubling its non-fossil fuel supply by 2035.

Emerging technologies such as green hydrogen, concentrated solar power and geothermal energy have also been folded into the blueprint, alongside next-generation energy storage solutions.

Over the next five years, China’s power grid investment is expected to exceed 5 trillion yuan (about 728.5 billion U.S. dollars), while efforts will continue to upgrade coal-fired power units for energy conservation and carbon reduction, and to promote technologies such as carbon capture, utilization and storage.

China’s push to build a new energy system carries significance well beyond its borders, as the rapid expansion of artificial intelligence data centers strains power grids worldwide and adds fresh pressure alongside growing climate concerns.

According to a February report from the International Energy Agency, global electricity demand is expected to grow at an average annual rate of 3.6 percent over the 2026-2030 period.

China’s technological and manufacturing edge is helping bridge this gap. The country has ranked first globally in new energy vehicle production and sales for 11 consecutive years, and it produces 80 percent of the world’s solar cells and 70 percent of both wind turbines and lithium batteries.

According to Xi, China’s new energy industry has made real progress in open competition and represents advanced production capacity, which not only increases global supply and alleviates the pressure of global inflation but also contributes significantly to global climate response and green transition.

“Low-carbon energy development concerns the future of humanity,” he has said, pledging that China stands ready to work with the international community to boost energy cooperation, safeguard energy security, address climate change, and protect the ecological environment to promote sustainable development and benefit people around the world.

The move follows a January 2025 decision to stop issuing licenses for new petrol-powered commercial motorcycles, commonly known as moto taxis, in the City of Kigali.

The directive applies to new entrants into the motorcycle taxi business, meaning that anyone seeking authorisation from the Rwanda Utilities Regulatory Authority (RURA) to operate as a moto taxi rider must use an electric motorcycle.

Speaking on the development, Amb. Uwihanganye said the policy is already delivering results and will soon be expanded beyond Kigali to cover the entire country.

“As you know, the government decided that passenger motorcycles must be electric, especially in the City of Kigali. In the coming days, we will scale up this measure to the national level. No motorcycle that is not electric will be allowed to enter the country, and this will apply to passenger motorcycles across Rwanda,” he said.

He noted that the market for electric motorcycles has matured significantly, making nationwide implementation possible.

“The market has already responded. There are importers bringing in motorcycles, and companies providing charging services. While everything may not yet be perfect, the sector has grown enough for us to expand the policy,” he added.

Statistics show that at least 14,031 motorcycles were sold in Rwanda in 2025, marking a 28 percent increase compared to the previous year.

A significant share of these were electric motorcycles, whose sales have surged by 686 percent since they were introduced in Rwanda, according to data from MotorcyclesData.

Under the policy, motorcycles already registered and operating on fuel will be allowed to continue their services. The restriction mainly targets new registrations of petrol- and diesel-powered motorcycles used for passenger transport.

Petrol-powered motorcycles are set to be phased out of Rwanda’s market.Spiro, an e-mobility company, is a dominant player in the Rwandan market.Ampersand is also gaining traction in the Rwandan market.

The Rwanda Development Board (RDB), together with private-sector stakeholders, held an engagement session with members of the Private Sector Federation (PSF) on Wednesday to discuss expectations and preparations for the upcoming Africa CEO Forum Annual Summit, scheduled for May 14–15, 2026, at the Kigali Convention Centre.

The summit, one of Africa’s leading platforms for high-level business dialogue and deal-making, is expected to bring together more than 2,000 chief executives, investors, policymakers and heads of state from over 75 countries.

Speaking during the engagement session, RDB Chief Executive Officer Jean-Guy Afrika said the forum presents a rare opportunity for Rwandan businesses to directly engage with leading African and global investors, financiers and decision-makers in one place.

“For Rwandan firms, the value of the forum is practical and immediate. It offers a rare opportunity to meet potential investors, identify strategic partners, open new commercial partnerships, and present concrete projects or expansion plans to decision-makers who are otherwise difficult to access in a single setting,” he said.

The Rwanda Development Board (RDB), together with private sector stakeholders, on Tuesday held an engagement session with members of the Private Sector Federation (PSF) to discuss expectations and preparations for the upcoming Africa CEO Forum Annual Summit.

Afrika noted that the forum goes beyond networking, providing businesses with a chance to benchmark themselves against leading firms across the continent, understand where capital is moving, and sharpen their growth ambitions.

He also highlighted the event’s advanced matchmaking technology, which allows registered participants to access profiles of investors, policymakers and financiers before the summit and request one-on-one meetings.

“They have coupled the forum with sophisticated matchmaking technology that suggests people who could be of interest to your business,” he said, urging businesses to register early and approach the event with clear targets and defined business goals.

“This is not a platform to attend passively. Firms should come prepared with clear objectives, targeted meetings, and a strong sense of what partnerships, capital, market access or commercial opportunities they want to pursue.”

This will be the third time Rwanda hosts the Africa CEO Forum, reinforcing Kigali’s growing role as a regional hub for investment, conferencing, tourism and business diplomacy.

The Africa CEO Forum is scheduled for May 14–15, 2026, at the Kigali Convention Centre.

Afrika said the organisers’ decision to return to Kigali reflects confidence in Rwanda’s logistics capacity and ability to host major continental events.

“This event is happening in Kigali for the third time because the organisers trust our ability, our logistics capabilities, and our ability to organise events of this scale,” he said.

He noted that Rwanda has sufficient conferencing and hospitality capacity and that authorities are closely monitoring registrations and visitor arrivals to ensure a smooth experience for delegates.

The 2026 summit will be held under the theme, “The Scale Imperative: Why Africa Must Embrace Shared Ownership,” with discussions expected to focus on business expansion, cross-border investment and regional integration.

The agenda will centre on three priorities: shared equity to promote multinational African firms, shared infrastructure to strengthen regional value chains, and shared frameworks aimed at harmonising regulations and standards across borders.

Various private sector stakeholders attended the meeting on Tuesday, April 22, 2026.

PSF urges businesses to prepare

Private Sector Federation Chairperson François Twagirumukiza said the forum, co-organised by Jeune Afrique Media Group and the International Finance Corporation (IFC), offers a strategic gateway for Rwandan businesses to move from ambition to execution.

“This forum matters because it provides a powerful gateway to new partners, new suppliers, new clients and new technologies. It connects our businesses to the networks and capabilities they need to grow significantly and compete,” he said.

He urged businesses to approach the summit with intent by identifying the partners they want to meet and booking meetings in advance.

“The value you derive will depend on the level of preparation you put in,” he said.

The Africa CEO Forum 2026 is expected to position Rwanda’s private sector at the centre of some of the continent’s most important investment conversations.

Businesses share past gains

Several business leaders shared testimonies of how previous editions of the Africa CEO Forum created tangible results for their companies.

Fabrice Shema, CEO and founder of Africa Medical Supplier Ltd, said attending the 2019 forum in Kigali helped him secure a $5 million in financing from a private investment fund without collateral requirements.

“I attended Africa CEO Forum 2019 here in Rwanda and it brought significant opportunities. I was able to connect with an institution that helped me secure $5 million in financing without providing collateral,” he revealed, adding, “That alone was a major milestone and gives us confidence that the 2026 edition will deliver even greater value.”

Julie Mutoni, Deputy Group CEO of Multilines International, said the last forum helped her logistics company secure new international partners and business leads that continue to support operations today.

“Through networking, I managed to get partners that I’m still working with today. In countries where I could not even reach, I was able to reach there through partnerships,” she said.

This will be the third time Rwanda is hosting the Africa CEO Forum.

For the 2026 edition, Mutoni said she is targeting more logistics partners across global markets as well as potential financing opportunities to expand and diversify her business.

“I’ll be looking at getting more partners, and depending on who is attending, I may also look for funding to expand my business. I’m just going to keep my eyes open and ensure that I grab the opportunities,” she said.

With President Paul Kagame, Nigerian President Bola Ahmed Tinubu and several other African leaders expected to attend, the Africa CEO Forum 2026 is expected to position Rwanda’s private sector at the centre of some of the continent’s most important investment conversations.

For many businesses, the goal is to turn two days of meetings in Kigali into partnerships and deals that last well beyond the summit itself.